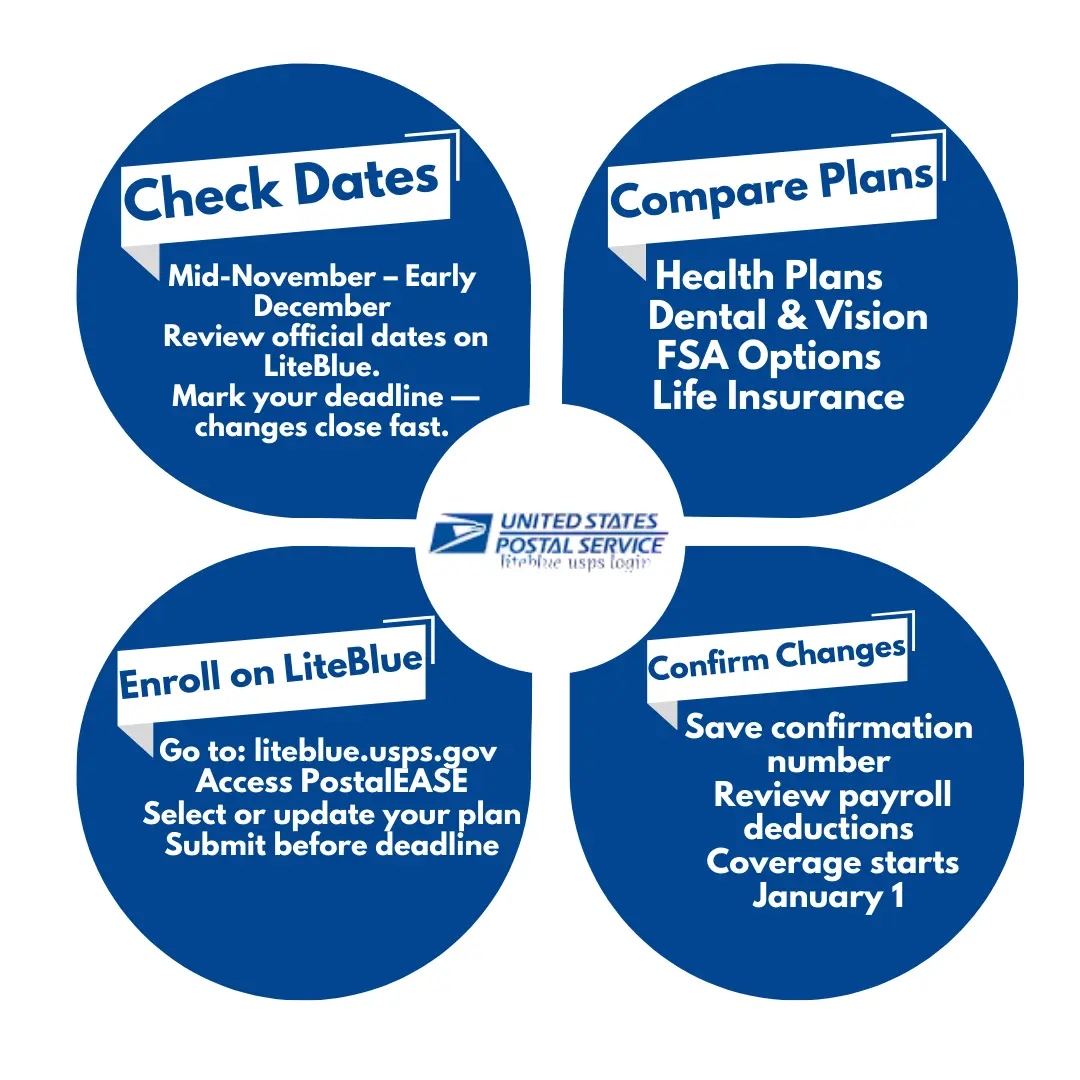

Every year, employees of the United States Postal Service are given an important opportunity to review and update their benefits through LiteBlue Open Season. While many employees focus on deadlines and enrollment steps, the most critical decision during this period is choosing the right health plan.

Selecting a health plan is not just about picking the cheapest option. It directly affects your monthly budget, medical coverage, family security, and long-term financial stability. With multiple plans available, each offering different benefits, costs, and provider networks, making the right choice requires careful evaluation.

This guide is designed to help USPS employees understand how to choose the best health plan during Open Season using a practical, step-by-step approach. It focuses on real decision-making factors, comparisons, and strategies to ensure you select a plan that truly meets your needs.

Understanding Health Plan Options in Open Season

During Open Season, USPS employees typically choose from federal health programs such as FEHB or PSHB, along with various provider options. Each category includes multiple providers offering different premium rates, deductibles, and coverage levels.

| Plan Type | Description | Best For |

|---|---|---|

| Self Only | Covers only the employee | Individuals |

| Self Plus One | Covers employee + one dependent | Couples |

| Self and Family | Covers entire family | Families with children |

Key Factors to Consider Before Choosing a Plan

Choosing the right health plan requires evaluating multiple aspects, not just monthly cost.

1. Monthly Premiums

The premium is the amount deducted from your paycheck. Lower premium plans may have higher out-of-pocket costs, while higher premium plans often offer better overall coverage.

2. Deductibles and Out-of-Pocket Costs

The deductible is the amount you pay before insurance starts covering expenses. Key terms to understand include the deductible itself, copay, coinsurance, and the out-of-pocket maximum — the total you will ever pay in a single year.

3. Coverage Scope

Check what services are included in each plan. Important areas to review are doctor visits, hospital stays, prescription drugs, preventive care, and specialist visits.

4. Network of Providers

Each plan has a network of doctors and hospitals. Ensure your preferred doctors are included and verify hospital availability in your area before committing to a plan.

5. Family Needs

If you have dependents, consider plans with strong pediatric care, maternity coverage, and accessible specialist options for all family members.

Step-by-Step Guide to Choosing the Best Plan

Step 1: Evaluate Your Current Health Needs

Start by analyzing your medical usage. Consider how often you visit doctors, whether you require regular medication, and whether you have any planned surgeries or treatments in the coming year.

Step 2: Review Your Current Plan

If you already have a plan, check last year's expenses, identify gaps in coverage, and compare existing benefits against new options available this Open Season.

Step 3: Compare Multiple Plans

Do not rely on a single plan. Compare at least 3–4 options side by side to get a clear picture of the tradeoffs between cost and coverage.

| Feature | Plan A | Plan B | Plan C |

|---|---|---|---|

| Monthly Premium | Low | Medium | High |

| Deductible | High | Medium | Low |

| Doctor Visits | Limited | Moderate | Extensive |

| Prescription Coverage | Basic | Good | Comprehensive |

Step 4: Calculate Total Annual Cost

Do not focus only on premiums. Factor in deductibles and your expected medical expenses throughout the year to get a true picture of what each plan will actually cost you.

Step 5: Check Flexibility

Look for plans that allow easy specialist access, out-of-network coverage, and flexible emergency care options. Flexibility becomes especially valuable in unexpected medical situations.

Common Mistakes to Avoid

Many employees make errors that cost them financially. The most frequent mistakes are choosing the cheapest plan without checking coverage, ignoring deductibles, not reviewing plan changes annually, overlooking family needs, and missing provider network details. Taking extra time to avoid these errors can save significant money over the course of a year.

Comparing Low vs High Premium Plans

Low Premium Plans

Lower monthly deductions make these plans suitable for generally healthy individuals. However, the tradeoffs are higher out-of-pocket costs when you do need care and potentially limited coverage overall.

High Premium Plans

These plans offer better coverage and lower out-of-pocket expenses when medical care is needed. The main downside is the higher monthly cost regardless of how much care you actually use.

How Your Choice Affects Your Salary

Health plan selection directly impacts your take-home pay. However, a lower premium plan may lead to higher medical expenses when care is needed, so the true financial impact depends on your actual usage throughout the year.

| Plan Type | Monthly Premium | Annual Cost |

|---|---|---|

| Basic Plan | $100 | $1,200 |

| Standard Plan | $250 | $3,000 |

| Premium Plan | $400 | $4,800 |

Special Considerations for Different Employees

For Single Employees

Lower premium plans may be sufficient for single employees in good health. Focus on ensuring adequate emergency coverage and prescription access as a minimum baseline.

For Families

Choose plans with strong pediatric and hospital coverage. Families with children or dependents who require regular care should consider higher premium plans for better protection and lower out-of-pocket exposure.

For Employees with Chronic Conditions

Prioritize plans with low deductibles and strong medication coverage. Employees managing ongoing conditions will typically benefit most from comprehensive plans despite the higher monthly cost.

Role of Preventive Care

Most plans offer preventive services at no additional cost, including annual checkups, vaccinations, and health screenings. Choosing a plan that supports preventive care can significantly reduce long-term medical costs by catching issues early.

How to Use Plan Comparison Tools Effectively

During Open Season, comparison tools are available on the benefits portal. Make the most of them by comparing benefits side by side, reviewing detailed cost breakdowns, and checking provider network availability for your area. These tools are designed to simplify the decision and should be your first step when evaluating options.

Advanced Strategy for Smart Selection

Combine Cost and Usage Analysis

Instead of guessing, calculate your expected doctor visits, medication costs, and likely emergency scenarios for the coming year. Then match these estimates with each plan's features to find the option with the lowest true total cost.

Long-Term Planning Considerations

Health plan selection should not be viewed as a short-term decision. Think about future medical needs, potential family growth, and aging-related healthcare requirements when evaluating which plan offers the best long-term value.

Frequently Asked Questions (FAQs)

Conclusion

Choosing the best health plan during Open Season is one of the most important financial and healthcare decisions for USPS employees. It requires a careful balance between cost, coverage, and personal needs.

By evaluating your health requirements, comparing available plans, and understanding long-term implications, you can make a well-informed decision that protects both your health and your finances. Rather than rushing through the selection process, take time to review all available options, analyze your situation, and choose a plan that offers the right level of security and value. A thoughtful decision during Open Season can provide peace of mind for the entire year ahead.